Auto Enrolment Enquiry

Speak To Us Today

To speak with one of our team about auto enrolment, please fill in your details below and pick a time that suits.

info@symmetryfinancial.ie

")

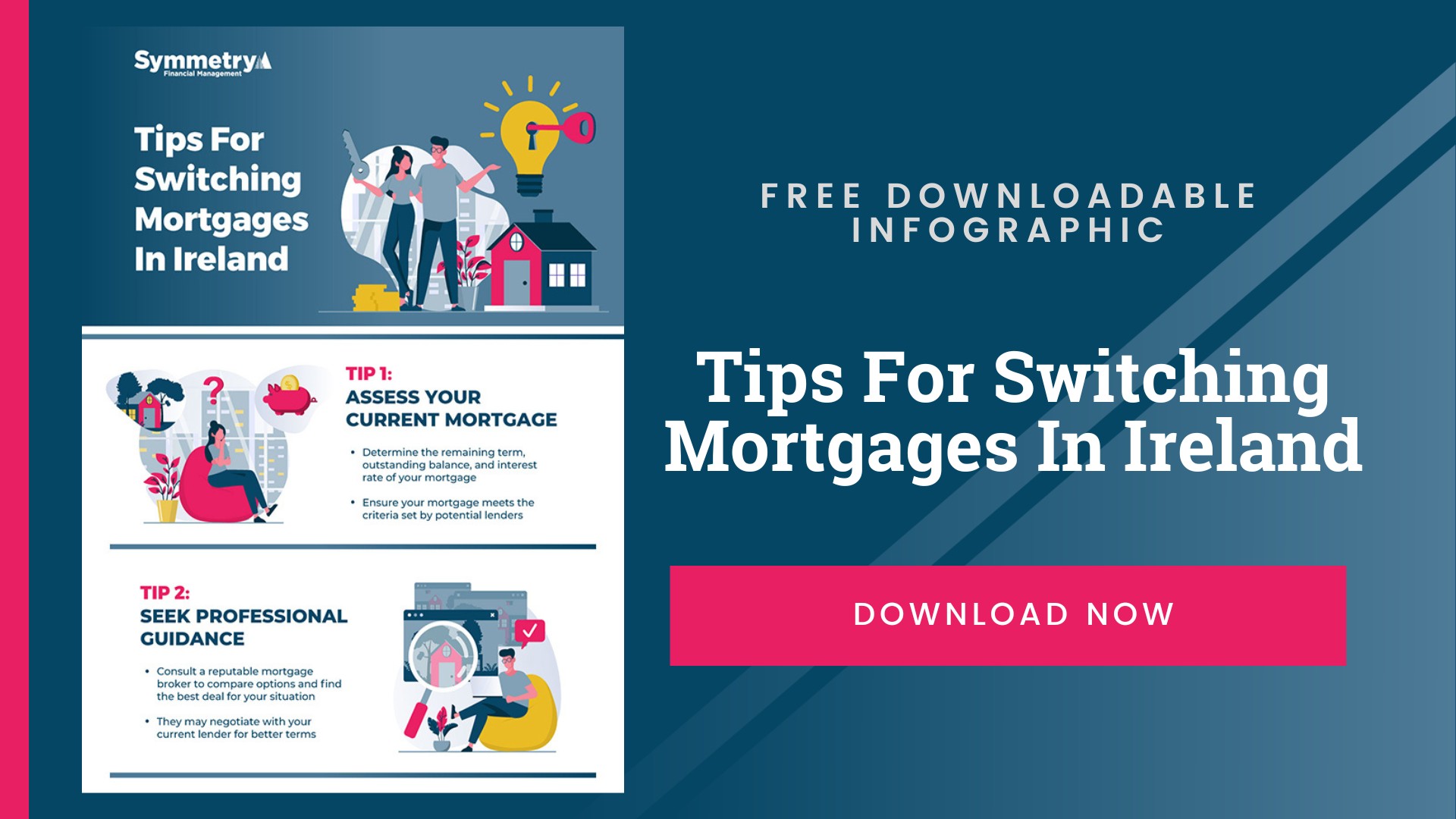

We’re all feeling the pinch as we navigate this cost of living crisis, so finding ways to reduce outgoings wherever possible is key, and opting for switching mortgages is one surefire way to make substantial savings.

Those that decide to jump ship to a different lender could reduce the cost of their mortgage by over €10,000. During a time of unprecedented inflation – or indeed, at any time – this is a significant amount that would be put to better use in a homeowner’s pocket.

If you’re considering making the switch but are unsure where to begin, read on to find out how to switch your mortgage in Ireland in six simple steps.

Before opting for a mortgage switch, it’s important to find out where you stand on a few key details which may affect the process. These include:

These are all crucial pieces of info, as some lenders will only accept mortgages with a term and an outstanding amount that exceeds a specific cap to ensure the switch is financially worthwhile. Furthermore, a fixed-rate mortgage may incur a penalty fee for an early exit, which is another potential issue to consider.

Seeking the help of professionals when comparing mortgages is highly advisable, as they will have the knowledge and experience to scout out the best deal for your circumstances. To secure this, they will check several criteria, such as competitive interest rates and cashback incentives.

However, their first port of call is likely to be a conversation with your current lender to see if they can bring a better deal to the table.

As with first-time mortgages, you will once again need to gather all the essential documents required to seal the new deal. You will be asked to provide:

Your new lender will require an up-to-date valuation of your property to help establish a more accurate loan-to-value (LTV) ratio. This valuation should be organised with a lender-approved valuer only. Your advisor will assist you on how to obtain this at the appropriate time.

Hiring an experienced solicitor is a vital part of the process. Your advisor can recommend a reputable solicitor from their panel.

Once the switch has been made and the legal pack signed, it’s time to tie up any loose ends regarding your original mortgage. For example, you will need to reassess your existing mortgage protection policy.

If there are no changes to the terms of your mortgage with your new lender, you don’t necessarily have to organise a new mortgage protection policy. However, it could be the perfect time to make further savings by searching for a better deal and reviewing your cover options to ensure that you and your family are protected.

Whatever course of action you decide to take, you will always need to inform your current policyholder of your change in circumstances, so they can adjust your policy details accordingly.

With so much to be gained from switching your mortgage, there has never been a better time to take the plunge. And with over 80 years of combined experience in the industry, there is no one better than Symmetry Financial Management to help you make the switch.

Our impartial, expert team are on hand to offer professional mortgage advice, helping you discover what options are available to you, which one best suits your needs and making the entire process as easy as possible.

Get in touch to schedule an appointment and allow us to help you secure a better deal today – and make significant savings in the process.

Also, don’t forget to head over to our blog and resources for more of the latest financial news and advice.

If you’d like a free, no-obligation consultation for your mortgage, pension or financial needs, get in touch here, call us on 01 6831673 or email us directly on info@symmetryfinancial.ie.

The Mortgage Process Explained